Many Americans think their economic future looks bad. But what does that actually mean? And how can we measure that? What are the best indicators for a quick understanding of the struggles of the American worker?

One of our recurring themes is that broad economic measures, like GDP or unemployment, do not give a true picture of the real economy. To fill that gap, we want to look at lesser-known measures of economic instability and precariousness: Emergency savings and living paycheck-to-paycheck.

This article is one of a series of stories looking at the best economic indicators and measures that capture the problem of economic insecurity. We want to look at two indicators in this article: the number of people who lack emergency savings and the number of people who live paycheck to paycheck.

Emergency Savings

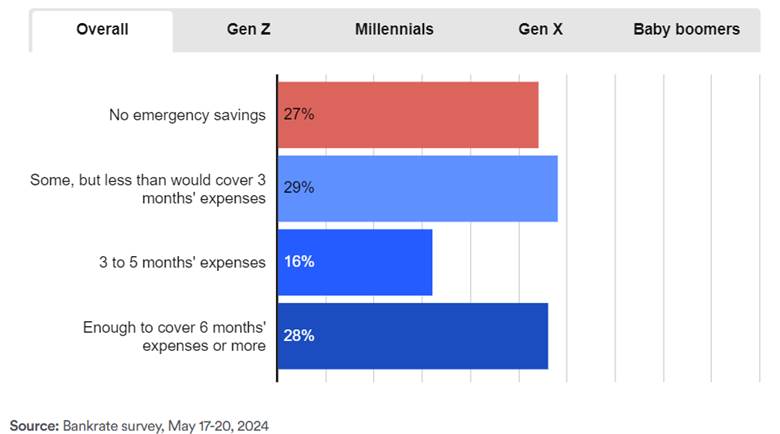

The 2024 Annual Emergency Savings Report from Bankrate, found that 27% said they had no emergency savings. 59% of people are uncomfortable with their level of emergency savings.

Emergency savings are defined as enough savings to cover 3 to 5 months of expenses if an emergency arises. They are used to cover important expenses such as job loss, a medical bill or a car repair bill without using credit card debit. Several companies and websites measure emergency savings, including Bankrate, a consumer finance company. They surveyed more an 1000 US adults each year on their savings.

According to the Bankrate survey, 56% of people do not have enough savings to cover an emergency expense.

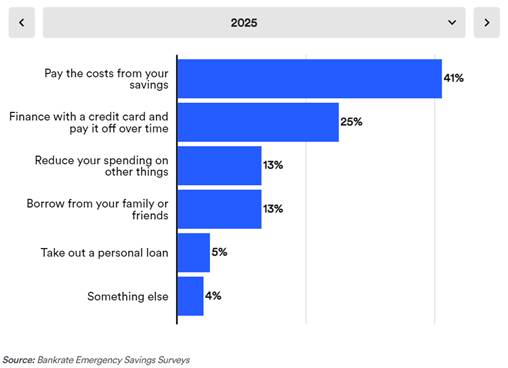

Second, the Bankrate survey also found that 1/3 of US adults had more credit card debt than emergency savings. The survey has some good news, 41% said they could pay off an unexpected expense of $1,000 from an emergency room visit or a car repair, from their savings.

The Federal Reserve also surveys Household Economic Well-being. The Federal reserve survey is more positive. The Fed found that 63% of people could pay an emergency expense of $400 dollars from cash. Sixteen (16%) percent would pay using a credit card.

In addition, 48% said they could pay an emergency expense of $2,000 or more.

The latest survey was conducted in 2023 and the results were published in 2024.

Living Paycheck to Paycheck(P2P)

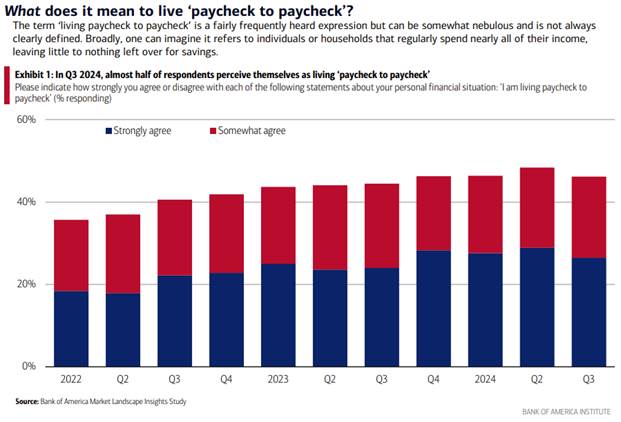

The number of people who say they live paycheck to paycheck is another important statistic to watch. Living paycheck to Paycheck is defined as having no money leftover for saving after supporting basic needs. The three surveys from Bank of America, Bankrate and LendingClub reported similar data: Between 34% to 57% of people live paycheck to paycheck according to surveys.

About 46% of people spend all of their income each month (Bank of America Institute). The graph is from this publication (Bank of America Institute)

About 57% percent of Americans say they live paycheck to paycheck. More than four in 10 (42%) Americans with household incomes of $100,000 or more say they live paycheck to paycheck. (Nerdwallet)

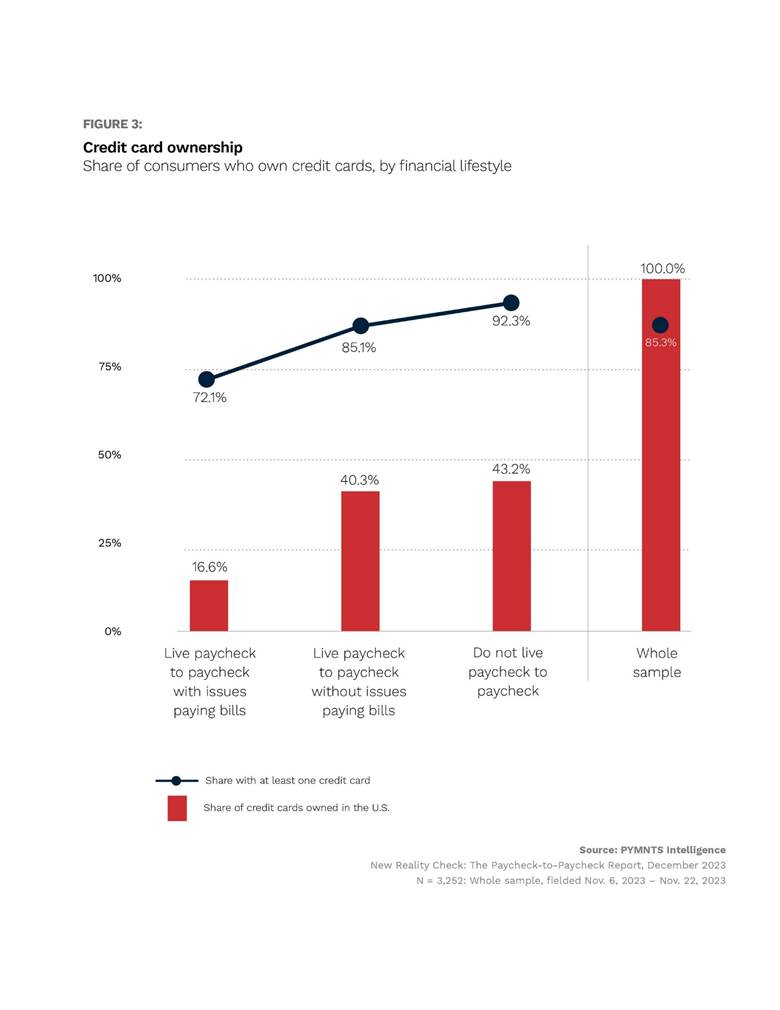

Lending Club also has a large survey that collects paycheck-to-paycheck data. They surveyed 3,252 credit card holders in 2023 regarding debt and expenses. LendingClub found that 62% of cardholders reported living paycheck to paycheck.

More interestingly, they also break down the data. Among those earning less than $50,000 dollars, they found 77% lived paycheck to paycheck while those with income of $50K to $100K reported P2P of 67% and $100K plus had a P2P rate of 45%.

Lending Club’s data provides particularly valuable insights by breaking down paycheck-to-paycheck living by income bracket:

- 77% of those earning under $50,000 live paycheck to paycheck

- 67% of those earning $50,000-$100,000 live paycheck to paycheck

- 45% of those earning over $100,000 live paycheck to paycheck

Our final survey is from Bankrate. They report that one in three workers (34%) live paycheck to paycheck.

These two indicators, we believe, give the best “snapshot” as to how the economy is doing for workers in the short-term.

These two indicators—emergency savings and paycheck-to-paycheck living—provide a more accurate snapshot of economic well-being than traditional macroeconomic measures. They reveal widespread financial vulnerability across income levels, even among those traditionally considered middle or upper-middle class.

When Americans lack financial buffers and exhaust their earnings before the next payday, they face constant economic insecurity despite what headline macro-economic numbers might suggest. The unemployment rate and the S&P 500 are not the real economy. These measures revel the challenges facing working Americans today.